![]()

How Inflation Could Impact Your Retirement Decisions

Submitted by MIRUS Financial Partners on April 19th, 2022

How could the value of a nickel worth $3.2 million go unrecognized for years? In 1962, collector George Walton was on his way to a coin show when he died in a car accident. His family inherited the rare Liberty Head Nickel and had it appraised. It was declared fake and stuffed in a drawer. But at the 2003 World’s Fair, the coin was reappraised and found to be real. Ten years later, the family sold it for $3.2 million. For decades, the rising value of the coin went unrecognized.

Similarly, the cumulative effects of inflation can go unrecognized in retirement. Inflation has spiked recently, but it hasn’t been talked about much for the last 10 years. While price changes are slight on a day-to-day basis, the effects are significant over time. Since retirement can last 30 years or more, let’s look at the impact inflation could have on the price of products and services and how your income will need to keep up.

First, Inflation’s Impact

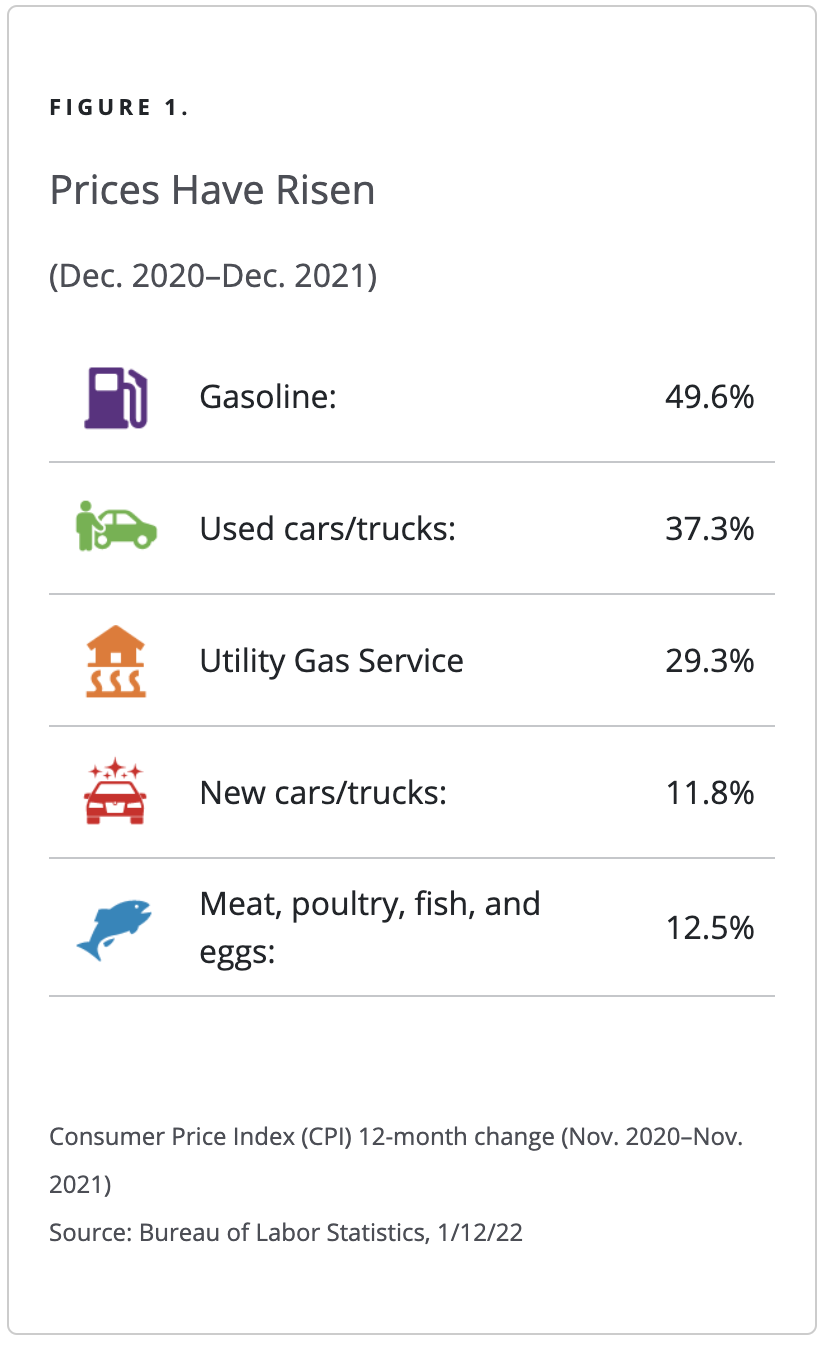

In January 2022, inflation was 7.5%—the highest it’s been in 40 years.1 It feels like a shock because, for the past 10 years, inflation has averaged only 2.1%.1 Prices haven’t increased equally for all products. For example, some prices have increased far more than 7.5% (see Figure 1).

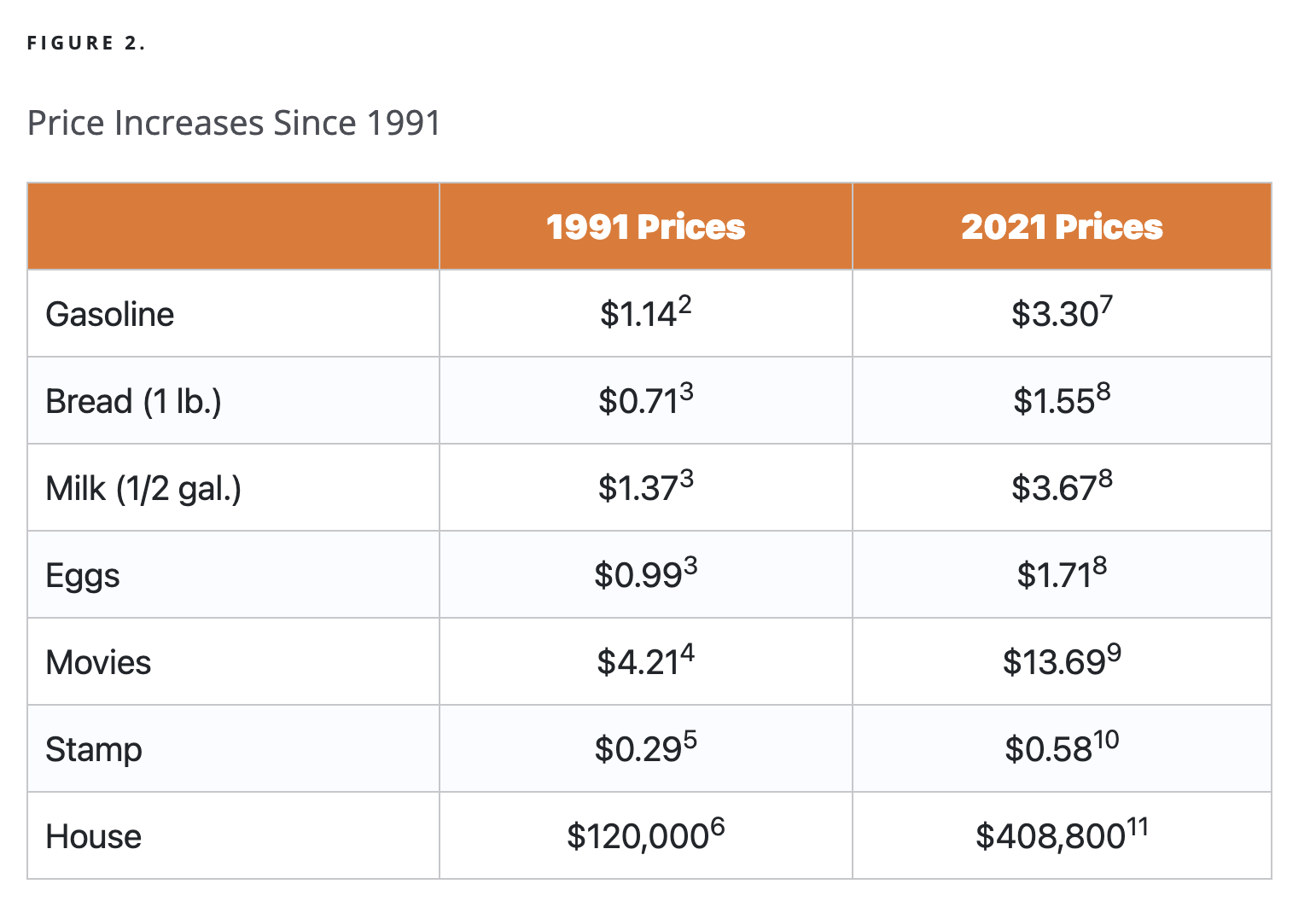

While inflation may not be this extreme in the future, it’s still something to think about. One way to consider the impact of future inflation on a 30-year retirement is to look back 30 years. Let’s compare prices from 1991 compared to prices in 2021 (see Figure 2).

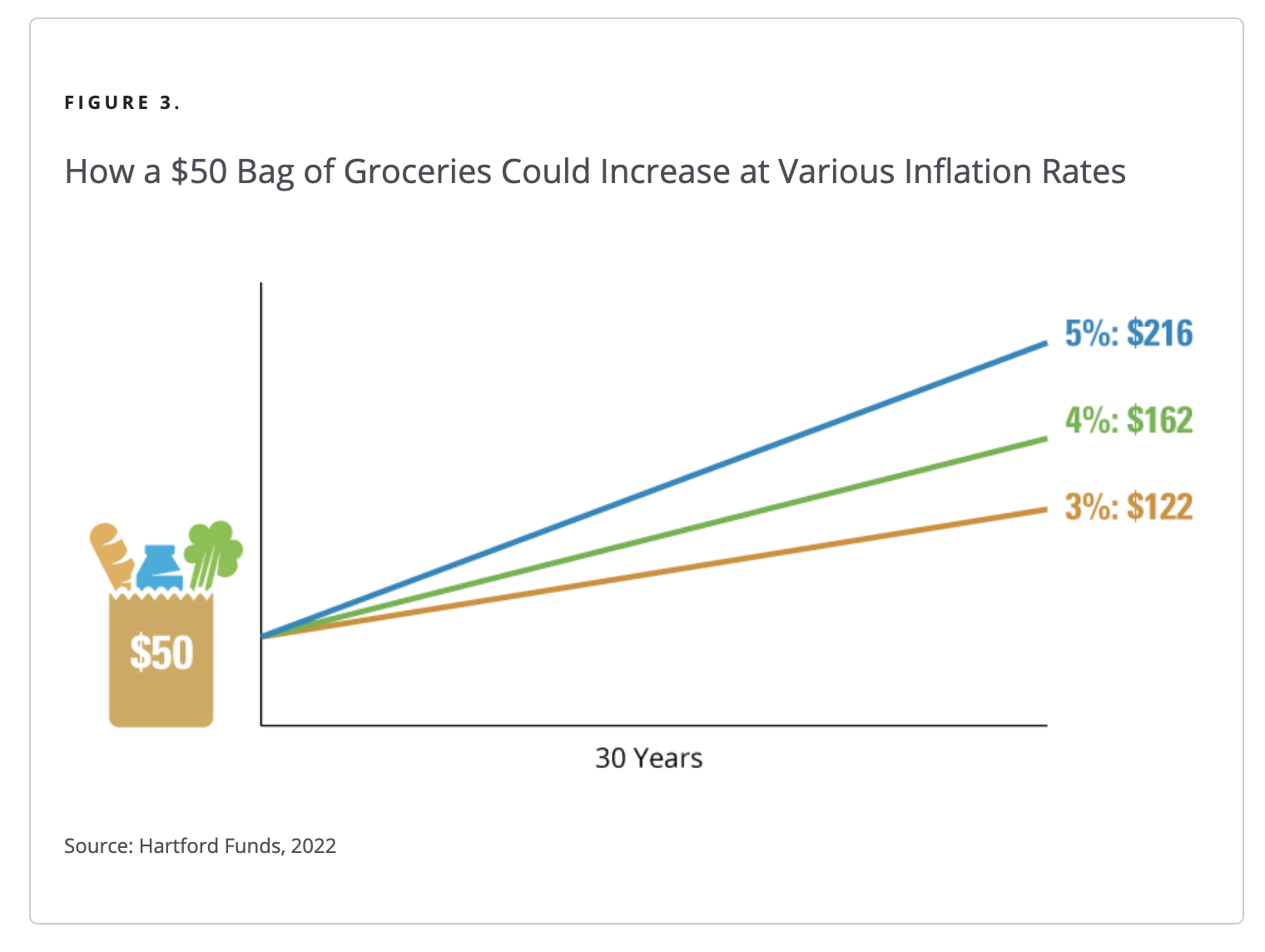

Over a few decades, even a little bit of inflation can have a big effect. If your retirement was to last 30 years, Figure 3 projects what today’s $50 bag of groceries today could cost in 30 years based on various inflation rates. Put another way, in 30 years at 3% inflation, you’d need $2.43 to buy what $1 could buy today.

Second, the Psychological Effects of Inflation

Lately, it’s been hard to avoid hearing about inflation. It’s been all over the news. According to a November 2021 Gallup poll, 45% of US adults said inflation is causing them financial hardship.12 So how can inflation affect our mindset as we approach, or are in, retirement? Many retirees rely on a fixed income, e.g., interest from bonds or CDs. As a result, they may be more vulnerable to inflation because their income may not increase enough to keep up with rising prices.

When products and services become less affordable, people can try to adjust by making fewer purchases or buying less expensive alternatives. They might also cut back on spending by giving up pastimes they enjoy. Unfortunately, this type of sacrifice comes with a cost of its own. It can make people feel anxious, insecure, and like they’re missing out on the good things in life.

If a retiree needs to withdraw more from savings to keep up with rising prices, their assets could begin to dwindle faster than expected. Doing so could raise fears about running out of money at some point in their retirement.

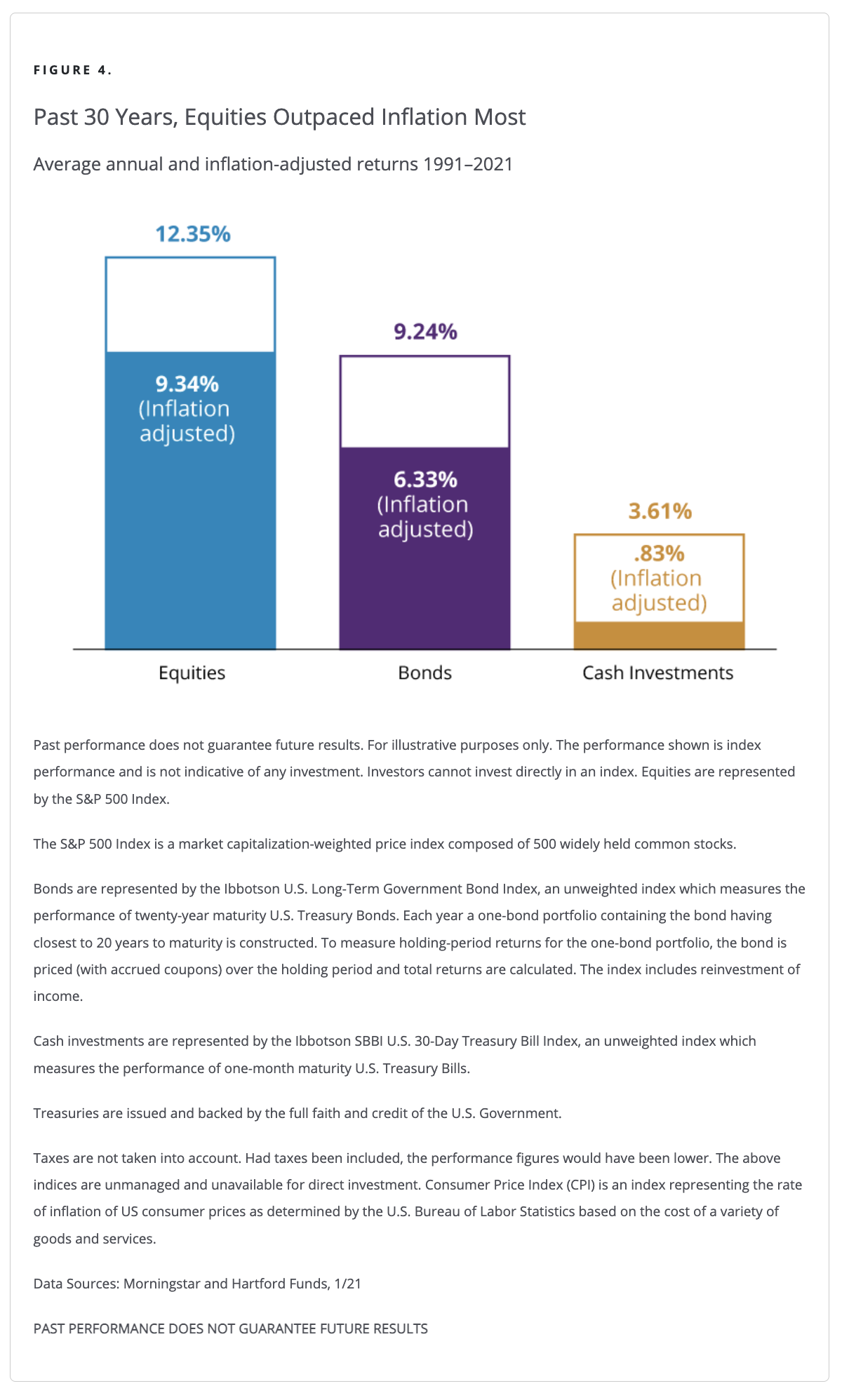

In retirement, many people think it’s best to invest less in stocks and more in investments perceived as “safe,” such as bonds, CDs, etc. Why? We may fear losses from stock-market volatility and the effect it could have on our income. But historically, over the long-term, fixed-income investments have provided lower returns than bonds and cash investments (see Figure 4).

As Figure 4 shows, over the last 30 years, equities have significantly outpaced inflation. The outpacing occurred despite six bear markets (market drops of more than 20%). The average drop of the six bear markets was 37% and the biggest drop was 52%.13

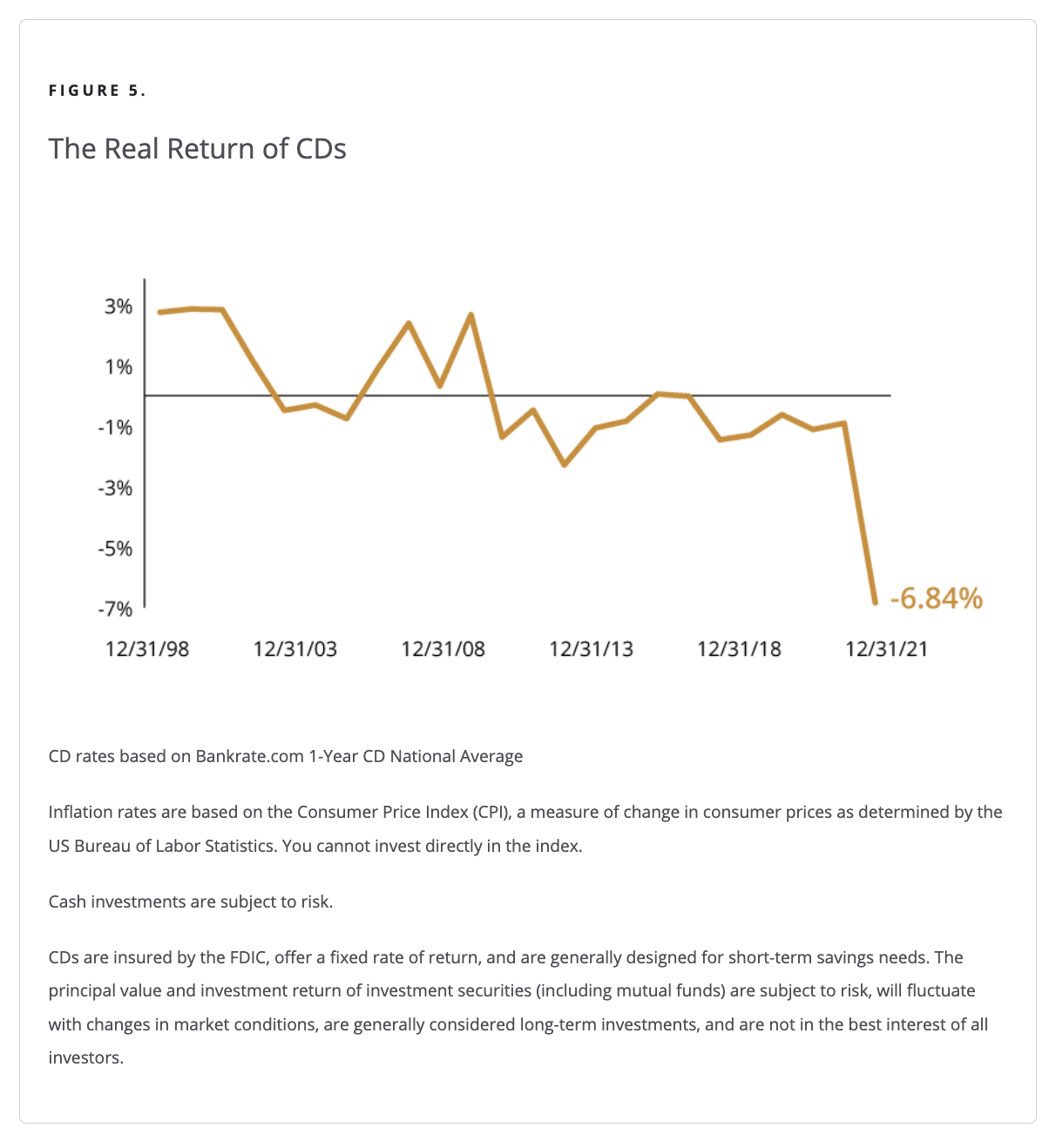

CDs can be especially attractive to retirees because they tend to be less volatile than equities or bonds. But when cash returns are adjusted for inflation, they can be less reassuring. The inflation-adjusted return of CDs has been negative for the past five years (see Figure 5).

A financial professional can help you determine a mix of equities, bonds, and cash tailored to meet your income needs for a 30-year retirement. They may also consider commodities, real estate investments, and other types of investments to help guard against inflation.

Delaying taking Social Security benefits could also help guard against inflation in retirement because every year you delay taking it, your benefit increases 8% each year up to age 70.14 Visit the Social Security website to see what your benefit could be at various ages, e.g., 62, 67, or 70.

“But Stocks Are Too Risky in Retirement”

Equities tend to be more volatile than fixed income. In the past 30 years, we experienced significant bear markets, including Black Monday in 1987, the dot-com bubble, the Great Recession, and a global pandemic. Each of these events triggered market drops of 30%. Yet, despite these drops, the S&P 500 Index rose from 326 points on January 2, 1991, to 4,766 on December 31, 2021. During that time, your income would have to rise about two and a half times to keep up with 3% inflation. The S&P 500 Index rose more than 10 times.

To Summarize

First, the average inflation rate for the past 10 years has been 2.1%. But in January 2022, inflation jumped to 7.5%. Second, when inflation is rising, we may feel the effect financially and psychologically. Third, the growth of equities has historically outpaced inflation.

We Haven’t Heard Much About Inflation for Decades

When inflation’s low, its effects are somewhat forgotten about, similar to George Walton’s nickel that was put away in a drawer. But over time, even low inflation can have a big impact on our cost of living. Retirees should work with a financial professional to choose investments that can keep pace with inflation.

1 Bureau of Labor Statistics, 2022

2 Here’s what a gallon of gas cost the year you were born, USA Today, 8/20/2018

3 The cost of goods the year you were born, Stacker, 11/17/20

4 From pocket change to nearly $10: The cost of a movie ticket the year you were born, 8/29/19

5 United States Postal Service, 2021

6 Here’s How Much a New Home Cost the Year You Were Born, GoBankingRates, 10/13/17

7 Gas Prices, AAA, 2021

8 Graphics for Economic News Releases, Bureau of Labor Statistics, 2022

9 Movie Theatre Prices, 2021

10 Postage Rate Increase, Stamps.com, 2021

11 Average sales price of new homes sold in the United States from 1965 to 2021, Statista, 2021

12 Inflation Causing Hardship for 45% of U.S. Households, Gallup, 12/2/21

13 Ned Davis Research, 2021

14 Social Security Administration, 2022

Investing involves risk, including the possible loss of principal.

• Fixed income security risks include credit, liquidity, call, duration, and interest-rate risk. As interest rates rise, bond prices generally fall.

• The value of the real estate of real estate-related securities may go down due to various factors, including but not limited to, the strength of the economy, amount of new construction, laws, and regulations, costs of real estate, availability of mortgages, and changes in interest rates.

• Investments in the commodities market and the natural-resource industry may increase the Fund’s liquidity risk, volatility, and risk of loss if adverse developments occur.

All information provided is for informational and educational purposes only and is not intended to provide investment, tax, accounting, or legal advice. As with all matters of an investment, tax, or legal nature, you should consult with a qualified tax or legal professional regarding your specific legal or tax situation, as applicable.